Should you chase an unpaid debt through a debt collector or go straight to a lawyer? The answer depends on the size and complexity of the debt — but for most business debts, the choice is clearer than you might think.

What each option actually does

A debt collector contacts your debtor by phone, letter, and email to pressure them into paying. They're regulated under the Australian Consumer Law and the ACCC/ASIC Debt Collection Guideline (RG 96). They can't provide legal advice, issue statutory demands, or commence court proceedings. If the debtor refuses to pay, the collector's options run out.

A debt recovery lawyer does everything a collector can do — plus everything they can't. That includes issuing a formal letter of demand, filing a statutory demand under s 459E of the Corporations Act 2001 (Cth), commencing court proceedings, and enforcing judgments through garnishee orders, writs of levy, or winding-up applications.

Side-by-side comparison

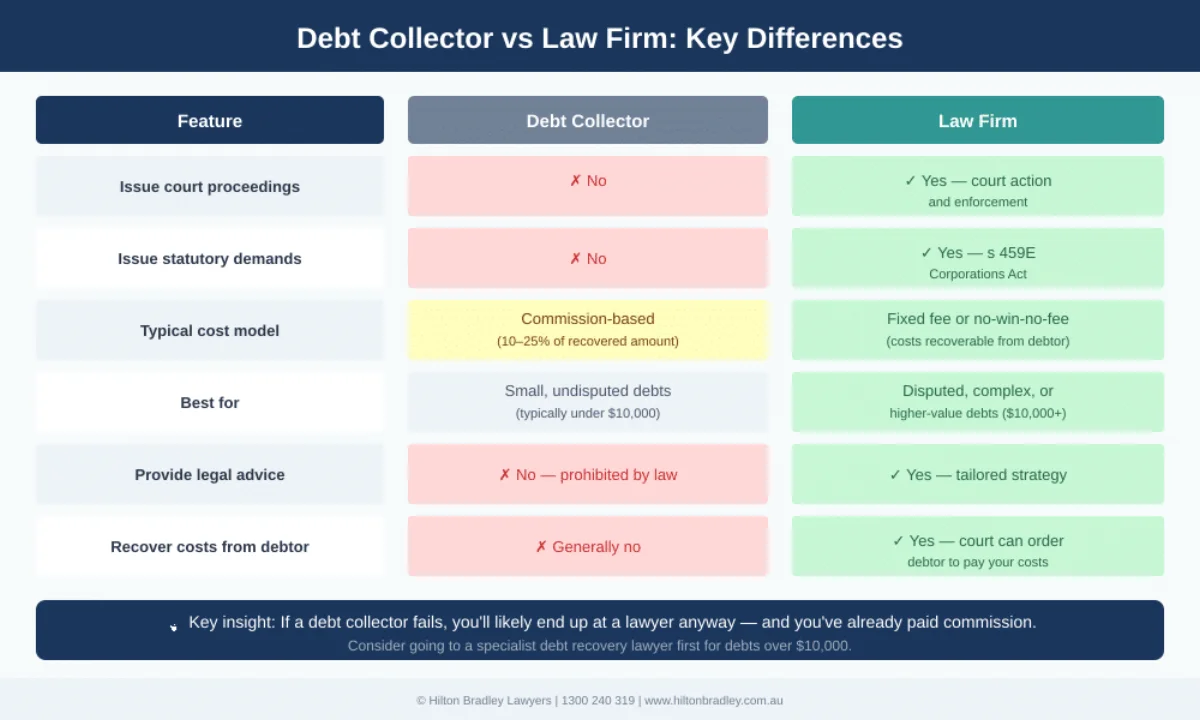

| Feature | Debt Collector | Law Firm |

|---|---|---|

| Issue court proceedings | No | Yes — court action and enforcement |

| Issue statutory demands | No | Yes — s 459E Corporations Act |

| Provide legal advice | Prohibited by law | Yes — tailored strategy |

| Typical cost model | Commission (10–25% of amount recovered) | Fixed fee or no-win-no-fee |

| Recover costs from debtor | Generally no | Yes — court can order debtor to pay your costs |

| Best for | Small, undisputed debts (under $10,000) | Disputed, complex, or higher-value debts ($10,000+) |

| If debtor still won't pay | Must refer to a lawyer | Can escalate directly to court proceedings |

How costs actually compare

On the surface, a debt collector's "no upfront cost" model looks attractive. But the commission structure means you lose a significant portion of your recovery. On a $50,000 debt, a 20% commission costs you $10,000 — and that's if the collector succeeds at all.

A debt recovery law firm typically charges a fixed fee for a letter of demand (often $200–$600), and if the matter escalates to a statutory demand or court proceedings, the legal costs can often be recovered from the debtor as part of the judgment. That means the debtor pays your legal costs — not you.

Consider this comparison on a $50,000 debt:

| Cost element | Debt Collector | Law Firm |

|---|---|---|

| Upfront cost | $0 | $0 (no-win-no-fee) or fixed fee |

| Commission on recovery | $7,500–$12,500 (15–25%) | $0 |

| Legal costs recovered from debtor | No | Yes (if court proceedings issued) |

| You receive | $37,500–$42,500 | Up to $50,000 |

The hidden cost of starting with a collector

Here's what most business owners don't consider: if a debt collector can't recover your money, you'll end up at a lawyer anyway. By then, you've lost months waiting for the collector to exhaust their process, potentially paid commission on partial recoveries, and given the debtor time to dissipate assets or become further insolvent.

Going to a specialist debt recovery lawyer first doesn't mean going to court first. A good lawyer will start with a letter of demand and negotiate before escalating. The difference is that if negotiation fails, they can escalate immediately — without the delay of changing providers.

When a debt collector makes sense

Debt collectors can be effective for high-volume, low-value consumer debts — think telecommunications companies chasing hundreds of $200 accounts. For these debts, the economics of engaging a lawyer for each matter don't stack up.

But for business-to-business debts — particularly those over $5,000 — a law firm is almost always the better option. The debtor takes a lawyer's letter more seriously, the escalation path is seamless, and you keep more of your recovery.

Key takeaways

- Debt collectors can only chase — they can't issue court proceedings, statutory demands, or provide legal advice

- Law firms do everything collectors do, plus everything they can't — from demand letters through to enforcement

- Collectors charge commissions of 10–25% on recoveries; law firms typically use fixed fees recoverable from the debtor

- Starting with a collector often means paying twice — once in commission, then again when you engage a lawyer after the collector fails

- For B2B debts over $5,000, a specialist debt recovery law firm is almost always the better choice

If your business is owed money and you want it recovered without commissions eating into your recovery, call Hilton Bradley on 1300 240 319 for a free consultation. We'll give you an honest assessment of your prospects and explain exactly how our process works.

Disclaimer: This article provides general information about debt recovery options under Australian law as at March 2026. It is not a substitute for legal advice specific to your situation. For advice tailored to your circumstances, contact Hilton Bradley on 1300 240 319.

Disclaimer: The information in this article is general in nature and should not be relied upon as legal advice. Please seek professional advice tailored to your particular circumstances.

Luke Whiffen

Founding Director

Luke is a founding director of Hilton Bradley with over 20 years' experience in insolvency and commercial litigation.

View profile →